Poor engagement in pensions and access to affordable financial advice has created a mammoth gap in savings that will leave people ill-equipped for retirement. As the urgency to close the gap intensifies, artificial intelligence (AI) is providing a much-needed solution.

A lack of engagement in financial services has resulted in a retirement savings gap that is growing at a worrying rate. Retirement naturally seems a great distance away for most of a person’s working life, which in an age of instant gratification has resulted in a general apathy towards pensions. Millennials, in particular, who already make up the majority of workers, are known to live in the moment rather than save for the future.

The issue also extends to the financial industry, which until the recent rise of fintech startups had done little to increase engagement with consumers because of a lack of market competition. With a small pool of large institutions having dominated the retirement market for a long time, there has not been enough incentive to invest in innovation and improving customer experience. This is now beginning to change as consumers demand an experience closer to digital services such as Netflix and Amazon.

Our mission is to create more engagement in financial services and to educate, engage and advise customers to build their own secure financial future

A recent report by the World Economic Forum (WEF) suggested that the average retired person in the UK will outlive his or her savings by more than ten years. In 2017, the WEF also estimated that if UK savings remained at their current level, the country’s retirement savings gap will grow from £8 trillion in 2016 to £33 trillion by 2050.

“The retirement savings gap is colossal,” says Fahd Rachidy, founder and chief executive of ABAKA, an AI-powered cloud-native platform for digital saving and retirement solutions that helps financial institutions provide accessible and affordable advice to consumers. “Governments are worried that if people don’t save enough money, they are going to have to foot the bill. We need to put the onus on industry and collectively we need to do more to help people save more.

“It’s a win-win situation for everyone. People save more and get a more secure financial future. Industry providers get more revenue on their top line. But it needs to happen now because the user experience involved in accessing your pension or increasing your contribution is ridiculous for the 21st century. Large providers are sitting on a huge number of legacy technologies, which are archaic and preventing them from innovating.”

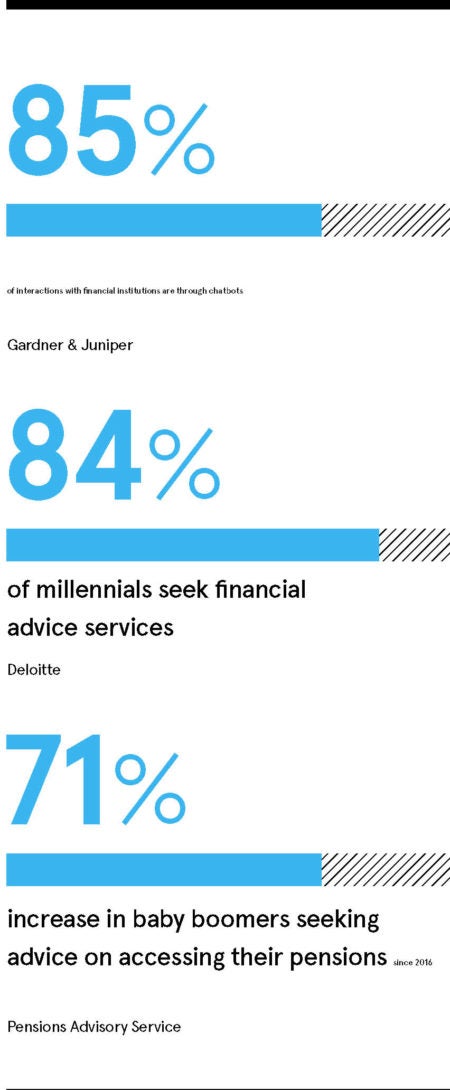

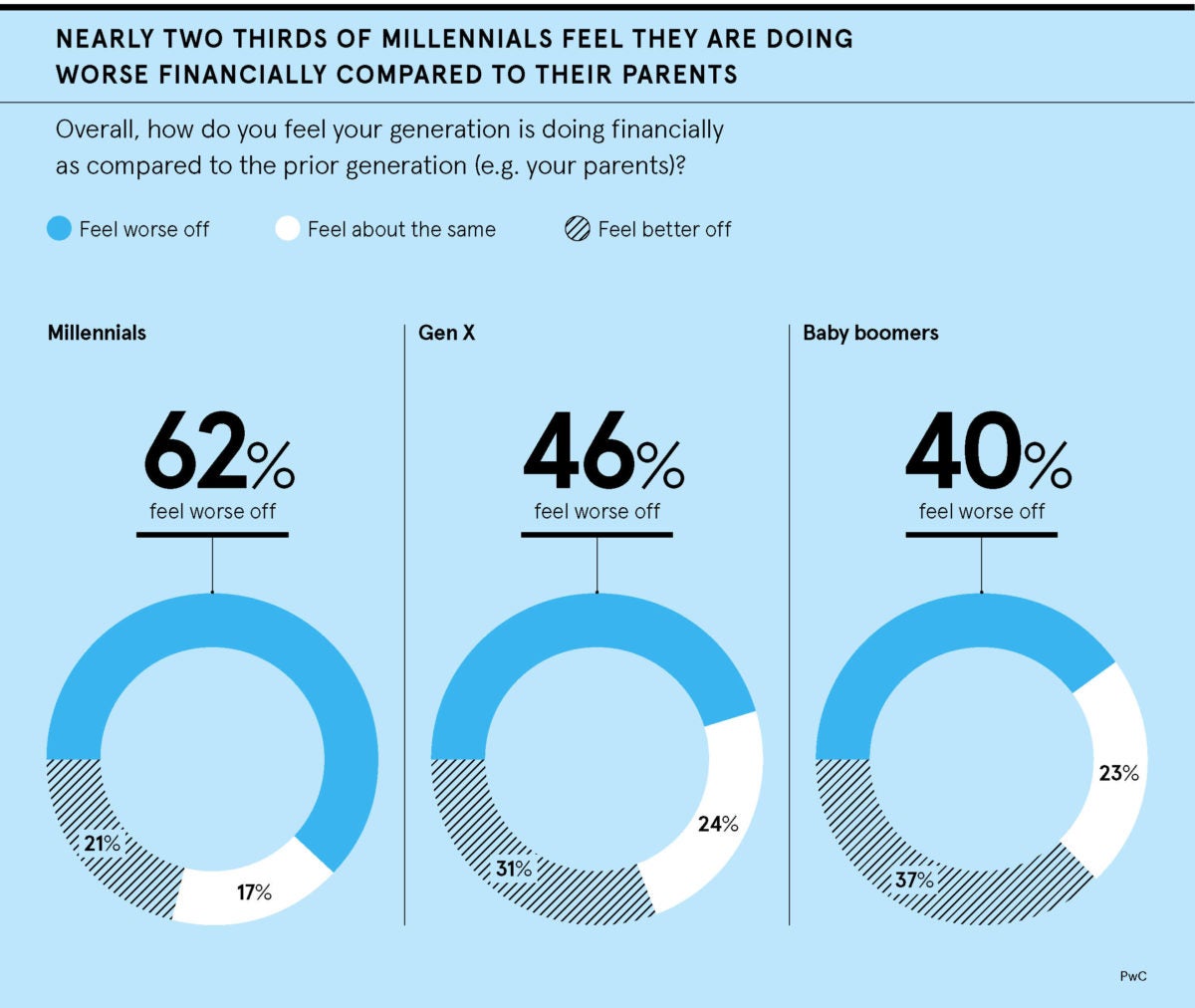

General awareness around pensions and retirement savings in the UK is woeful. More than a third of the adult population in the UK say they have no pension at all, rising to 55 per cent among millennials, according to a study by Finder.com and OnePoll. Of those who said they do have a pension, 36 per cent didn’t know how much was actually in it.

Perhaps most worryingly, 43 per cent of those quizzed in the study said they had no idea what a healthy pension pot looks like. Of those that did estimate, the average response was £174,000, despite Royal London recommending a pension pot of at least £260,000 if you want to avoid an uncomfortable retirement. Mr Rachidy was inspired to start ABAKA having witnessed his own father’s challenges in saving for retirement.

“My dad never had a pension and I think a lot of people today will end up like him if they don’t do anything today,” he says. “We come from a place where we always had to worry about money. That can be very stressful. When you spend your whole life working, at some point you want to take some time off and perhaps enjoy a holiday with your family. When my dad was looking for financial help, he couldn’t find it.

“He turned to his bank and to providers, but they weren’t interested because he didn’t meet the criteria of having enough money. Advice was not accessible and even if you could find it, it wasn’t affordable. That’s still a challenge today; there is a clear advice gap. It’s worrying that 90 per cent of the working population in the UK is not on track to achieve just a basic retirement income to cover their living expenses. We’re determined to change that and think the best way to do it is to help the industry transform itself and deliver outstanding and hyper-personalised customer experiences.”

ABAKA harnesses Artificial Financial IntelligenceTM to revolutionise how organisations financially plan for their clients. It has created an AI-driven digital platform that gives the financial services industry the means to better engage with their clients. The software platform consists of a library of modular, scalable applications designed to integrate with an organisation’s systems and business requirements. Financial institutions can use the modules and applications to build their own solutions and customer experiences.

Those modules include innovations such as conversational AI, intelligent personalised nudges, data aggregation technology and pension tracing consolidation. True conversational AI, otherwise known as chatbots, is a particular game-changer for engagement, according to Mr Rachidy, because it fills the advice gap by providing instant access to information on pensions, savings and investments through humanlike conversations.

“Instead of having to wait months for information from your provider, you can instantly talk to a robot online,” he says. “We are the UK’s first conversational AI platform in this space and we are delivering our solution across multiple markets now, in Asia, the US and Europe. Studies are showing more and more people are using chatbots and specifically for financial services. Once you’ve had this experience you don’t want to go back.”

ABAKA refers to the application of machine-learning in financial services as Artificial Financial Intelligence, and believes it will revolutionise the industry and help close the gap in retirement savings. Financial services are especially ripe for AI innovation because of the vast amount of transactional and behavioural information that providers collect on their customers. If leveraged in the right way with the right technology, this information can be used to enhance engagement and help people plan and save better particularly through actionable intelligent nudges.

As well as providing more affordable and accessible advice to consumers, Artificial Financial Intelligence also empowers advisers by allowing them to service more clients, even those who don’t meet their normal commercial criteria, in addition to helping large pension providers and retail banks to provide a solution at scale to the mass market.

“It’s data driven and creates better understanding of your customers, more opportunities for providers to service those customers and greater trust between all parties involved in retirement planning,” says Mr Rachidy. “Artificial Financial Intelligence is the future. Our mission is to create more engagement in financial services and to educate, engage and advise customers to build their own secure financial future.”

For more information please visit www.abaka.me