CLICK HERE TO DOWNLOAD AN EXCLUSIVE MONEY2020 EUROPE AGENDA PREVIEW

The financial services sector is going through unprecedented change, its commercial models profoundly impacted by the proliferation of technology and the changing expectations of its users. In addition, the barriers to entry are reducing due to regulatory initiatives – the Payment Services Directive II, Single Euro Payments Area and Single Digital Market Strategy to name a few – and this is creating a plethora of opportunities.

When this is combined with the fallout from the financial crisis, which has created an increased level of complexity for the incumbents, it’s clear to see that the financial services market is in a state of flux never before seen in the sector.

Opportunities for startups within financial services have never been greater, especially in the application of new technologies to improve upon existing services and models, and to overcome legacy challenges, whether technology, processes or people. Across Europe, a number of initiatives have sprung up to drive the development of startups within the sector, many of which have taken inspiration from the success achieved in Silicon Valley.

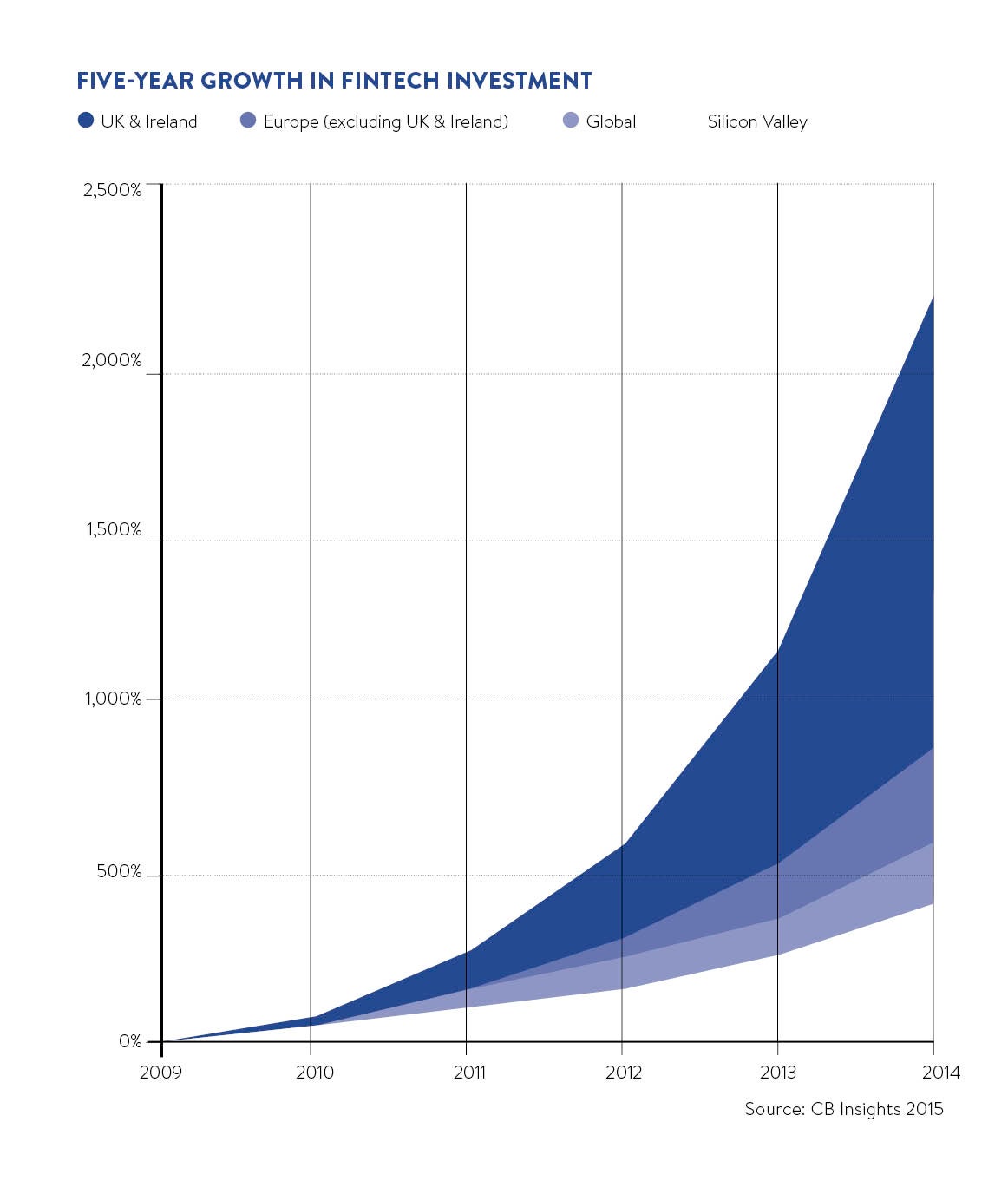

Lessons from Silicon Valley

While Silicon Valley is the most famous technology hub in the world, it has taken decades to achieve this status. When the computer chip industry was emerging in the mid-1950s, there were no venture capital investors in the area. The main university in the vicinity, Stanford, did not produce any research on computer chip components and the supply of local employees qualified to work with these high-tech devices was almost non-existent.

It all started when a small group of ambitious entrepreneurs, the founders of Fairchild Semiconductors, created the first successful chip company in the Bay Area. Co-founder Gordon Moor later claimed: “Every time we came up with a new idea, we spawned two or three companies trying to exploit it.”

Investment in the area has grown enormously over the years, as has collaboration between established companies, universities and the local ecosystem. Support from established entrepreneurs has played a key role in developing the “fail fast, fail often” mentality, which has created a risk-taking culture. A great deal of this success has been achieved without government support.

Creating a safe haven for innovation

In contrast, The Monetary Authority of Singapore (MAS), having committed S$225 million over the coming five years under its Financial Sector Technology and Innovation scheme, is developing a regulatory sandbox to provide a controlled experiment space for financial technology (fintech) startups. There are similarities with the UK Financial Conduct Authority’s “regulatory sandbox” initiative, which will allow businesses to test out new financial products and services without incurring all the normal regulatory consequences of engaging in those activities.

The MAS initiative has a slightly different goal as the intention of its sandbox is to create a safe space for innovation within which the consequences of failure can be contained. It will allow fintech startups to test their products in a live environment and to demonstrate a working concept to investors. MAS will also provide guidance and support to help startups develop their propositions, and navigate the barriers to market entry.

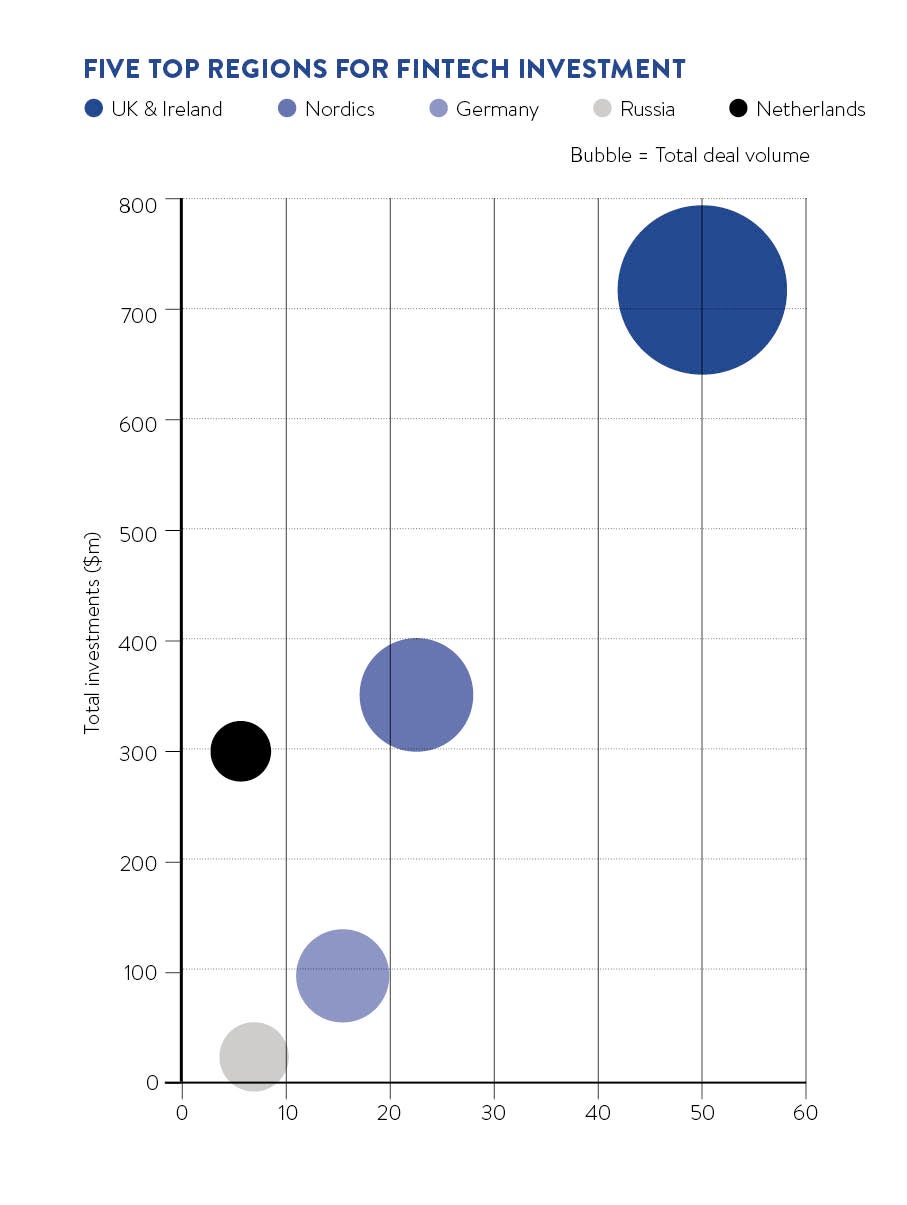

In London, initiatives such as Level39, Silicon Roundabout and Tech City have become the focal point for fintech companies. Level39 in particular continues to attract fintech outfits from around the world, with more than 200 member companies that are capitalising on London’s potential as a beachhead into mainland Europe, while also leveraging the City’s strong financial services heritage.

Many of the incumbent financial services institutions have created a variety of different investment vehicles and innovation labs within the City, which is boosting activity. One such company is UBS, a leading wealth management institution, that has set up an innovation lab to explore financial solutions based on new technologies, such as blockchain, which many industry insiders predict will revolutionise the sector. The City is now experiencing a growth in companies developing solutions to tackle regulatory and compliance issues, platform and API-driven propositions.

[embed_related]

European Initiatives

In Denmark, the strategic vision for Copenhagen Fintech Innovation and Research this year is to see the city grow as a recognised Nordic fintech hub bringing together existing players, universities and startups. Again, one of the key areas of growth is the application of blockchain technologies to solve industry problems. While corporates are trying to figure out how to improve their solutions by rebuilding on blockchain technology, but are hampered by legacy processes and systems, agile startups launching in this space are seizing the day.

Denmark has a special tradition for co-operation across sectors and this has influenced the financial services sector. Recent examples of collaboration between incumbents and fintechs are Danske Bank’s collaboration with Trifork in the development of Mobile Pay, and Nordea’s collaboration with Shopbox to develop small-business banking solutions.

The time of collaborative disruption is beginning as established financial services companies collaborate with startups to accelerate the pace of innovation

The Frankfurt-based initiative main incubator continues to reach its goal by identifying and capitalising on fintech trends to help shape the sector. This involved attracting investments for innovative fintech companies, and supporting them to grow stronger to strengthen Germany’s and continental Europe’s financial services sector. To date, main incubator has invested in four fintech companies, with further deals in the pipeline. It has started to build companies to help kick-start the local ecosystem and has successfully established the monthly Between the Towers event to create a dialogue between entrepreneurs and corporates, and a platform where ideas can be shared and developed.

Within 18 months, Holland Fintech has attracted more than 130 member companies and connected over 3,000 people in the broader sector. Collaboration is a key pillar of its strategy as there is an active focus to improve co-operation with numerous stakeholders such as government, regulators, other hubs and fintech companies around the world. It has witnessed a number of corporates experimenting in a variety of different ways and these collaborations are beginning to achieve some success, for example Rabobank with MyOrder and Facturis, ABN AMRO with Tink, or ING with Kabbage and R3 CEV. The insurance sector is a focus within the broader financial services space, and is being fuelled by investments and a greater appetite for experimentation and collaboration.

This wave of initiatives across Europe is beginning to yield results, creating hotspots for real innovation to develop. Collaboration between incumbents and startups, and regulatory support are essential to move to the next level. The time of collaborative disruption is beginning as established financial services companies collaborate with startups to accelerate the pace of innovation. This benefits both as the established companies are able to move more quickly through their more agile startup partners, while the startups gain access to investment, network and customers. Culturally, Europe has always lagged behind the United States in its appetite for risk – but in the future of fintech, he who dares wins.

CLICK HERE TO DOWNLOAD AN EXCLUSIVE MONEY2020 EUROPE AGENDA PREVIEW

Lessons from Silicon Valley

Creating a safe haven for innovation