What exactly is Facebook up to regarding cryptocurrencies? Earlier this month, Facebook updated its advertising policy to include a clause on financial services. “Ads must not promote financial products and services that are associated with binary options, initial coin offerings or cryptocurrency,” according to Rob Leathern, a product management director at the social network. “We want people to continue to discover and learn about new products and services through Facebook ads without fear of scams or deception.”

And yet Facebook’s board of directors includes investors such as Peter Thiel and Marc Andreessen who are crypto-evangelists, and in January Facebook’s founder Mark Zuckerberg mused about starting a Facebook cryptocurrency. In his “2018 Year Ahead” post, he explained that users are concerned about big-tech companies and spying governments. As part of his desire to win back trust, he speculated Facebook might adopt what he called “important counter-trends… like encryption or cryptocurrency” which “take power from centralised systems and put it back into people’s hands”.

It’s ground Mr Zuckerberg has trodden before, but it hasn’t proved successful. Back in 2009, the company launched Facebook Credits, a virtual currency for buying in-game items and non-gaming applications on the site. In January 2011, Facebook told all Facebook game developers they would have to process all payments through Facebook Credits from July 2011.

It’s ground Mr Zuckerberg has trodden before, but it hasn’t proved successful. Back in 2009, the company launched Facebook Credits, a virtual currency for buying in-game items and non-gaming applications on the site. In January 2011, Facebook told all Facebook game developers they would have to process all payments through Facebook Credits from July 2011.

The problem, according to Peter Vogel, co-founder and chief executive of online-offline loyalty programme Plink, is that Facebook misunderstood its own users. “Facebook experimented with ways to encourage adoption, giving away Credits to some users and offering a highly discounted rate on a first purchase of Credit, but these efforts didn’t encourage sharing and users were not allowed to give Facebook Credits to their friends,” he says. In 2012, Facebook stopped using Credits and in 2013 the virtual currency was officially removed from the site.

The company is still keen on payments – in December 2017, Facebook introduced a peer-to-peer payment option in its Indian version of WhatsApp – and analysts think a cryptocurrency would solve the key sharing problem because cryptocurrencies, the best known of which is bitcoin, work on a sharing system called blockchain.

Blockchain is the technology that allows bitcoin to function, originally invented by the mysterious coin-chain creator Satoshi Nakamoto in 2009. In essence, it’s a giant decentralised electronic ledger with duplicate copies on thousands of computers around the world. This number of duplicates means transactions can’t be altered retrospectively, so in effect it’s an irrefutable ledger that allows ownership and transfer of assets without the need for trusted third parties.

Sir Mark Walport, the government’s chief scientific adviser, believes the real-world uses of blockchain could stretch from “helping governments collect taxes, deliver benefits, issue passports, record land registries, assure the supply chain of goods, and generally ensure the integrity of government records and services… to helping protect the internet of things”. It could even be used to transfer patient health records and monitor the position of a driverless car.

Startups have been quick to realise what this means: traceability. London-based Everledger, for instance, uses the distributed ledger to track individual diamonds from the mine to the consumer, helping detect conflict diamonds and combat insurance fraud. Chief executive Leanne Kemp says they’re “putting bling on the blockchain” and more than 980,000 diamonds have been registered since its 2015 launch. The company plans to expand into the art world, which will bring it into competition with Berlin-based Ascribe, which was launched to help artists claim ownership of their work as it spreads online.

A social media cryptocurrency would move this form of transaction from the fringes of the internet into the mainstream

A social media cryptocurrency would move this form of transaction from the fringes of the internet into the mainstream via the billions of people who use social networks around the world. In China, social network WeChat hosts apps within its app, so that users click through to buy using channels entirely controlled by the brand, which offers unique experiences and simple payments. Daniel Murray, co-founder of fashion m-commerce startup Grabble, says this sidesteps the problem of getting your app on to a shopper’s phone. “No one downloads apps any more,” he says. “But 89 per cent of all time spent on mobile is spent in apps, so something is wrong.”

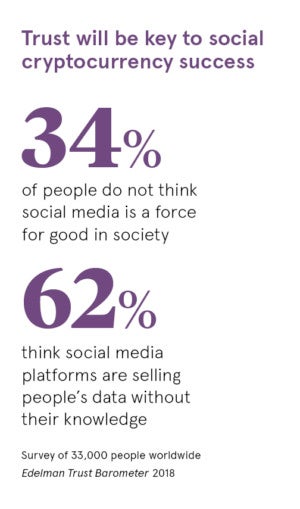

In an age where trust is faltering, millennials especially have trusted social media platforms and tech giants; they have been comfortable sharing pictures, intimate thoughts and much of their lives online, so it could be a natural progression to trust them to perform financial transactions.

But trust in social platforms may have been eroded by what is probably Facebook’s biggest crisis yet with boss Mr Zuckerberg admitting the giant social network “made mistakes” that led to millions of Facebook users having their data exploited by a political consultancy. A “breach of trust” had occurred, said Mr Zuckerberg.

Facebook now faces an uphill climb to rebuild its reputation and regain trust, but if it were to launch a cryptocurrency, the results could change the way the internet does business. “Facebook, with over two billion monthly active users, can basically drive the mass adoption of anything,” according to Clement Thibault, senior analyst at Investing.com.

And Facebook isn’t alone. Google’s parent company Alphabet has started investing heavily in fintech and crypto-startups. GV, Alphabet’s venture capital fund, recently invested $25 million in London-based cross-border payments provider Currencycloud.

E-Corp, the fictional tech conglomerate from USA Network’s Mr Robot, launched the E-Coin digital currency to extend its monopoly on everything from computers to consumer credit

Twitter chief executive Jack Dorsey, meanwhile, has invested in Lightning Labs, which is building its own version of blockchain, and rumours that Amazon has plans for its own coin have been circulating since late-2017. This followed a series of crypto-related domain name registrations made by Amazon’s legal department in October when the company acquired AmazonEthereum.com, AmazonCryptocurrency.com and AmazonCryptocurrencies.com.

There are many problems ahead. “Blockchain and distributed ledgers have the potential to revolutionise international payments,” explains Currencycloud co-founder Steve Lemon. “We’re already seeing smart applications using a blockchain as an alternative to traditional payment rails in hard-to-do and illiquid corridors, but it will take time before these technologies are used en masse because they are still too slow and illiquid.”

Paul Unterberg, vice president of product management at Prudential Financial, argues: “Bitcoin was created as a trust-free currency – just like a central bank-backed currency, you don’t need to trust the other party – and it’s by definition decentralised, so there’s no point of failure. A corporation’s coin would be the opposite – it would be centralised and require users to trust the company that issues it.”

And trust is easily lost. USA Network’s hacker drama Mr Robot features E-Coin, Evil Corp’s attempt at issuing a US dollar-equivalent digital currency. Evil Corp has a monopoly on pretty much everything, rather like the big five tech giants right now. Is it safe to put more power in their hands?

According to Karen Pepper, head of UK at Amazon Pay: “Millennials want shops with in-store technology to operate seamlessly alongside online, so bricks-and-mortar stores need to embrace online payment platforms like Amazon Pay.” But Grabble’s Mr Murray counters that this could actually cause more confusion. “Amazon are famously tricky with data and that has to stop if an Amazon coin were to progress,” he claims. “It’s their duty to provide transparent data to business customers.”

There is one possible solution, according to Yonatan Ben Shimon, chief executive and founder of cryptocurrency-social activity company Matchpool, who believes collaboration with existing experts is crucial for success. “To do it right, Facebook would have to be with a partner from the crypto space that understands how to build it in a decentralised way,” he says, seemingly throwing Matchpool’s hat into the ring.