Examination of the investment returns received by UK private clients during 2016 would appear to undermine the contention that we are living in a low-return environment.

According to the private client indices (PCIs) produced by Guernsey-based Asset Risk Consultants (ARC), sterling-based investors enjoyed a good year during 2016.

All four PCIs, which are based on the performance of more than 100,000 portfolios managed by 69 UK and Channel Islands-based private client investment management firms, generated strong returns during the year.

The ARC Sterling Cautious PCI, which has a risk relative to world equities of between 0 and 40 per cent, produced a return of 5.1 per cent, while the ARC Sterling Balanced Asset PCI, with a risk relative to world equities of between 40 per cent and 60 per cent, generated 8.6 per cent. The ARC Sterling Steady Growth PCI, with a relative risk of between 60 per cent and 80 per cent, posted 12.0 per cent; the ARC Sterling Equity Risk PCI, with a relative risk of 80 per cent to 110 per cent, recorded 14.8 per cent.

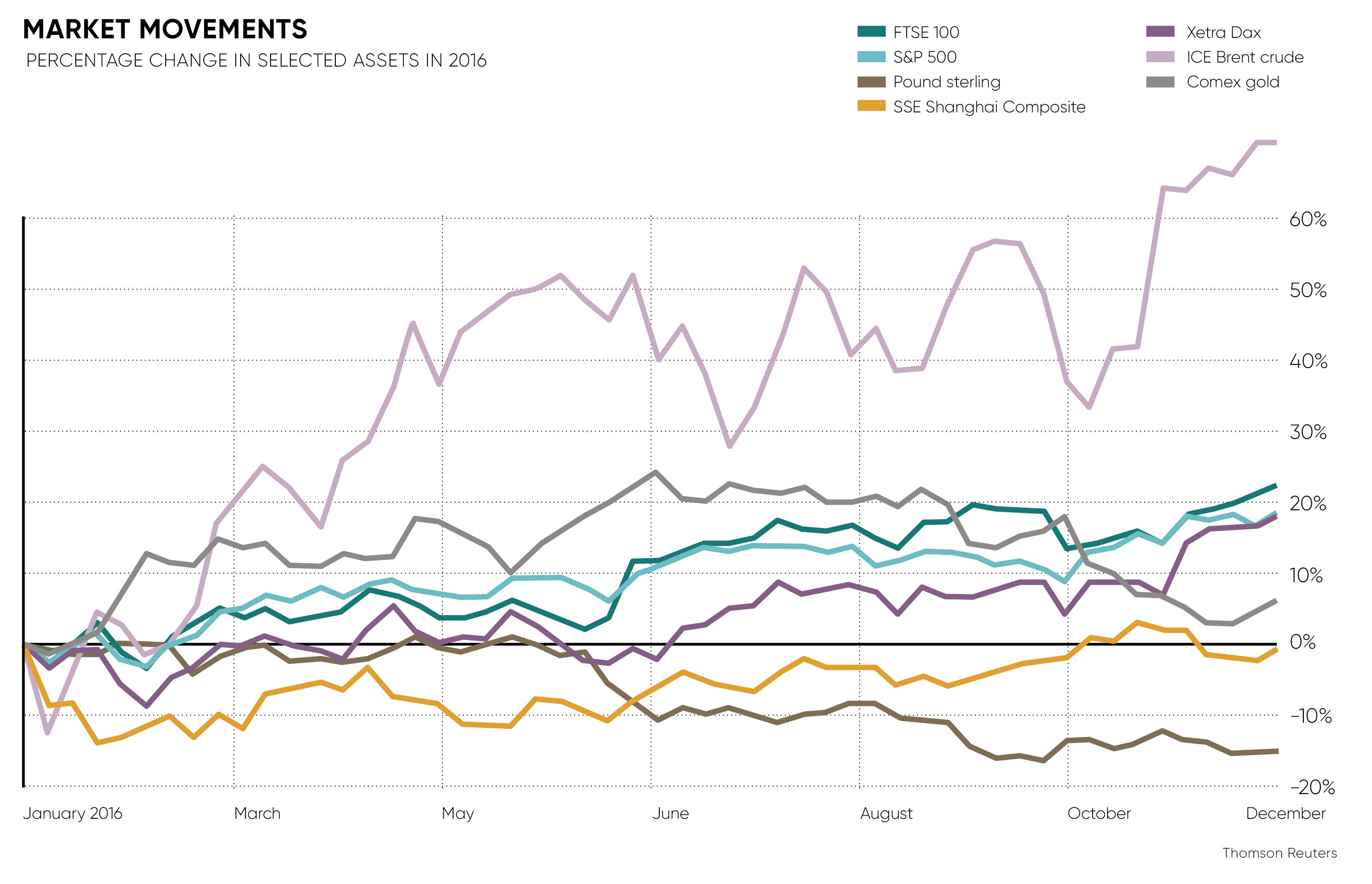

These returns appear all the more impressive given the turmoil that financial markets experienced during the first six weeks of 2016 when global equities fell by around 11 per cent.

By the end of March, however, global equity markets had recovered most, if not all, of these losses. They then surged ahead, ignoring in the process the potential setbacks posed by the shock result of the Brexit referendum in June and Donald Trump’s victory in the US presidential election in November.

Indeed, anyone who held the sterling-based MSCI World Index during 2016, rather than the more diversified multi-asset class portfolios that private client investment managers tend to provide, would have enjoyed a return of 25.62 per cent.

The realities

Unfortunately, however, these figures do not tell the whole story as far as investment returns are concerned both in 2016 and over the longer-term.

A significant proportion of the returns enjoyed by sterling-based investors reflected favourable foreign exchange movements, not least a depreciation of the pound by more than 15 per cent on a trade-weighted basis during the year to its lowest level since 1990.

The wealth of sterling-based investors may have increased on a local currency basis. But the international buying power of their wealth fell significantly. Furthermore, the ARC PCI returns for 2016 are significantly higher than the longer-term average.

The ARC Sterling Cautious PCI has generated an annualised return of 4.4 per cent since its inception in 2004, the ARC Sterling Balanced PCI 5.5 per cent, the ARC Sterling Steady Growth PCI 6.4 per cent and the ARC Sterling Equity Risk PCI 7.2 per cent.

On this basis, moving forward into 2017, it seems rather unlikely that sterling-based private investors will receive the returns experienced during 2016. Nonetheless, returns could still be positive in both nominal and real terms.

“Private investors should expect an ongoing abundance of gloomy prognoses, but a good chance of another respectable inflation-beating outcome for balanced portfolios,” says Kevin Gardiner, Rothschild Wealth Management’s global investment strategist.

For Mr Gardiner the most obvious risks are political, not least in the United States. “A new and idiosyncratic president of the United States is calling into question many long-standing assumptions about how the world works, and his protectionist instincts are indeed unsettling. However, it is not yet clear how they will be put into practice, nor what US trading partners’ responses will be. And any US tax cuts could be positively expansionary. We advise keeping an open mind,” he says.

Equities still look good value, although bonds are expensive. “Global stock markets have risen further, but do not yet look especially expensive – profits are reviving,” he continues. “We advise using setbacks as an opportunity to add to or to build long-term positions. Bonds, however, do look pricey. With little inflation, yet, they may remain so for a while and talk of a ‘bubble’ seems overly alarmist. But we doubt that many bonds will preserve investors’ real wealth from here.”

Both Coutts and Kleinwort Hambros are also sanguine about prospects going forward. Mouhammed Choukeir, Kleinwort Hambros chief investment officer, points out that markets have a habit of surmounting uncertainty and dire predictions. Over the past five years, global equities have appreciated by 55.6 per cent. While returns may be more difficult to achieve, they will not disappear, says Mr Choukeir.

“Not too long ago, cash in a savings account yielded 5 per cent; today equities may struggle to achieve that,” he says. “Still opportunities are ever-present. When they arise investors should maximise them. Increasing dispersion in market returns simply means investors should be more careful and discerning than in the recent past.”

Private investors should expect an ongoing abundance of gloomy prognoses, but a good chance of another respectable inflation-beating outcome for balanced portfolios

According to Mohammad Syed, a Coutts managing director, and head of financial advice and investment solutions, sterling’s recent depreciation, short-dated credit, financial debt, European equities, global healthcare and US technology should all provide useful sources of portfolio returns.

UBS Wealth Management, one of the world’s biggest wealth managers, also highlights the challenges posed by generating returns of more than 5 per cent a year in the current investment environment.

Investing in riskier assets, such as emerging market equities, adding leverage or seeking alternative risk premiums through exposure to “alternative” investments and hedge funds, provides one solution, although it may not be necessarily be appropriate for all sterling-based private client investors.

Investment managers and strategists tend to be optimists by nature. As far as private client portfolio returns are concerned, this optimism is reflected in most of their forecasts for 2017. As usual, time will tell.