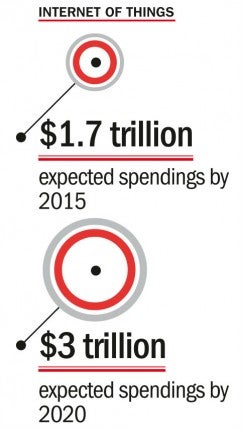

The promise of the eagerly anticipated internet of things (IoT) is exhausting to think about. Connected objects are soon to outnumber people on this planet, with analysts predicting a 30 per cent increase on 2014 numbers to 4.9 billion this year. IoT spending is expected to exceed $1.7 trillion in 2015, rising to $3 trillion by 2020. Despite this, we have not yet entered a truly connected era.

To date we have pockets of activity. Bank customers, for example, expect the same level of customer experience across all internet-connected devices as they would when stepping into a physical bank. Elsewhere, the connected home has started to become a reality, putting thermostats, lighting, entertainment and security at the touch of your finger.

But in the main, as useful as it may be to connect your Bluetooth toothbrush to your phone, these levels of connectedness do not yet affect us to our core. Were the toothbrush connected to our bank balance through a chain that includes our phone and our dental insurance, then Colgate would have our full attention.

Such instances of usage-based insurance are springing up, most notably in the automotive insurance industry with telematics products such as Drive Like A Girl by InsureTheBox, but these are isolated instances of partnerships rather than fully fledged digital communities.

We have seen all too often that doing “digital” means a social media campaign or a flash new website; at best it’s a bolt-on to an existing service to beef up the company’s competences and keep up with the rapid development of technology.

Any organisation can engage with customers 24/7 across digital channels, but this is only scratching the surface of a truly digital offering. Rarely has a business revolutionised to put IoT at the core of its service. The result is a siloed customer experience that will excel in one area, but may disappoint in another.

The key to retaining customers and gaining new ones in this age of eroded customer confidence is being able to provide a brand new customer experience that will keep up with the crest of the IoT tidal wave. By minimising the need to look elsewhere, customers are saved both time and money, and grow dramatically in affiliation to the provider.

But this is no mean feat when considering the size, speed and complexity of the wave. The world is changing too fast for any one organisation, no matter how large, to do everything by itself.

The only way for an organisation to provide even richer services and handle the resulting complexity, while reducing cost, is to highly automate and integrate key enabling services from within the organisation and a wider ecosystem of complementary partners.

The world is changing too fast for any one organisation, no matter how large, to do everything by itself

Such new service bundles test the limit of existing business architectures and technology platforms as organisations will be able to aggregate key competencies, orchestrate those into a multi-service offering and provide the operational support required to enable a greater customer experience from cradle to grave – product development to customer service and operations.

Here a business can operate simultaneously in a business-to-business, business-to-consumer and business-to-business-to-consumer world, as services are shared and delivered between businesses, and the final product “assembled” and billed to the customer under one brand.

The result is an offering that counts go-to-market time in days rather than months and is able to take complete ownership of its customer relationship. Not only are middle men cut out, placing brand positioning firmly back in the company’s hands, but customer loyalty will rocket through product innovation and value creation.

This value add is particularly vital in highly commoditised industries, such as retail banking or insurance, where a race to the bottom brought on by comparison websites or innovative financial technology startups has been proving costly in recent times.

At BearingPoint, we see wearable technologies as a further opportunity to strengthen customer relationships. Devices such as payment wristbands or health trackers will come and go, even if integrated in something as smart as Apple’s iWatch. But the power lies in combining data from previously unconnected sources – internal, external or even open data – to create customer insights that can inspire new types of financial products.

For example, it is easy to see the impact of gym, supermarket and travel activity on health insurance. By building into wearables a gym pass, supermarket loyalty card and travel card that includes cycle networks, banks would be at the core of a person’s day and, by teaming up with an insurance provider, can adjust premiums accordingly.

The race is already on to build up big data and advanced analytics capabilities to power such new product development. A recent BearingPoint Institute research paper cited 71 per cent of surveyed insurance companies were set to make big data and advanced analytics their maximum priority by 2018, but 73 per cent admit to a status of either “lagging” or “emerging” on the maturity scale.

Banks are largely further ahead, some even engaging with customers through open application programme interfaces that enable customers to take control of their own data. French bank Crédit Agricole delivered an industry first with its mobile app store, CAStore, launching more than 20 applications in less than two years.

Alongside this opportunity comes great responsibility. The financial services sector is still suffering from low customer confidence and reputational damage. It is a much-needed stroke of good fortune that the key global business trend of this generation leads to enhanced customer centricity offering companies the chance to regain ownership of customer relationships.

However, financial services players will have to work hard to prove they can be trusted with a relationship as intimate as the one collaborative platforms are set to facilitate. If ethically sound and robust measures are shown to be of the highest priority, customers will hand over ever more parts of their life in search of convenience and consistency. From our experience, this is one example where you really can “build it and they will come”.

To read more about the connected digital economy, please go to http://bit.ly/instODE