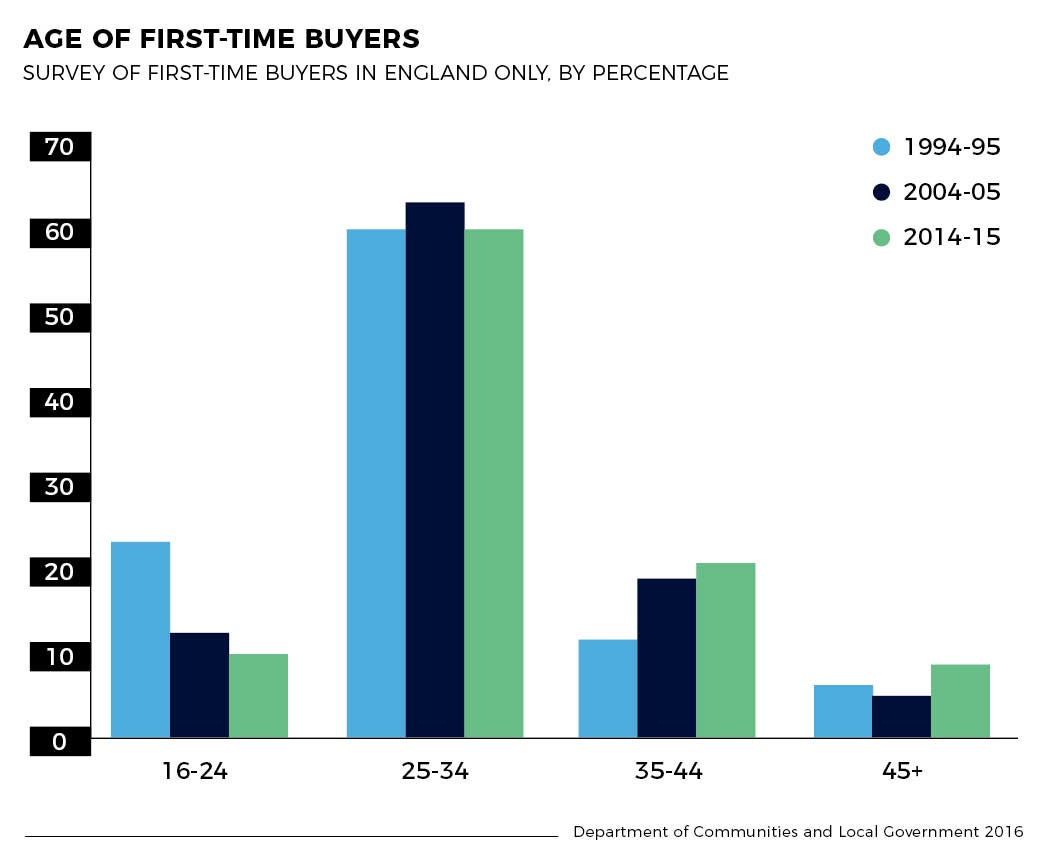

The first rung of the property ladder seems increasingly beyond reach, with the cost of houses in the UK now standing at around six times the average salary.

House prices have soared by around a fifth over the past three years, while salaries rose by just 6 per cent over the same time period, according to latest figures from Nationwide. At the same time the average value of a home in the UK has jumped to an all-time high of £222,484, says Halifax.

However, there are options to help wannabe first-time buyers trying to scrape enough together for a deposit in 2017.

First time buyer tips

Buying a first home typically means saving a deposit of around 10 per cent, or more to access the best mortgage rates. This involves setting aside tens of thousands of pounds, but there are various government schemes that may offer a helping hand.

For example, the Help to Buy equity loan scheme slashes the deposit needed to 5 per cent and offers an interest-free loan for a further 20 per cent from the government. This scheme can be used to buy new-build properties in England worth up to £600,000, and is available to buyers until 2020.

Despite some uncertainty, many experts predict prices will keep rising, even if at a slower pace

First-time buyers saving for a house deposit may also want to consider the Lifetime ISA, available from April 2017. Savers aged between 18 and 40 will get £1 from the government for each £4 they put into the ISA before they turn 50. A maximum of £4,000 can be saved into the ISA each year, topped up to £5,000. This can be used to buy a first home worth up to £450,000 anywhere in the UK.

Despite some uncertainty over how the housing market will perform in 2017, many experts predict prices will keep rising, even if at a slower pace. If you are determined to buy a first home, consider where you can slash spending to help reach this target.

As an example of how to budget, you could set aside 50 per cent of income after tax for essential spending, and a maximum of 30 per cent towards nights out and holidays. The balance, at 20 per cent, can be put towards savings for life goals such as buying a first home. However, the more you can save, the better. There are plenty of online budgeting tools that can help.

Saving tools

Scouring bank statements is a starting point, checking where spending can be reduced. Are there any utility bills that may be cut by switching provider, for example, or would you be wiling to ditch the TV package? Keeping a steady eye on spending habits will also help when getting a mortgage. Providers tend to carefully consider mortgage applicants’ spending patterns, following tougher affordability tests introduced in April 2014.

With the Bank of England’s base rate at an all-time low of 0.25 per cent, it can seem pointless hoping for any worthwhile interest on your savings. However, it’s still worth comparing the many accounts on the market as rates vary widely. Using comparison services is a first step to securing the best deal.

Buying a first home typically means saving a deposit of around 10 per cent, or more to access the best mortgage rates

Saving into an account on a monthly basis can pay. Some banks offer regular savings accounts with interest rates significantly higher than other rates on the market, at up to around 5 per cent. However, you’ll have to stick to the rules for the best deals. These typically include having a current account with the bank, and there are caps on how much you can save each month.

Fixed-rate accounts also offer higher rates, but these involve tying up your cash for a specific period, which may not suit anyone saving for a deposit to buy. Beware of ‘bonus rates’ on savings accounts, which typically applies for a period of around 12 months, and once this ends interest payments may sink dramatically. Make a note in your diary of when the bonus expires, so you can move your money if necessary.

Also remember to check the conditions, as even some ‘easy access’ accounts limit the number of withdrawals you can make each year.

Other options for first time buyers

Be flexible and consider all options that may reduce the sum required to buy, particularly while house prices continue to rise well above wage inflation. Many first-time buyers are unable to rely on the bank of mum and dad, but perhaps buying with a friend is an option for some. Up to four people can legally be registered as co-owners of a property, although how the purchase is structured needs careful consideration.

Alternatively, there are shared ownership schemes, enabling someone to buy a portion of a home and pay rent on the remainder.

If you are currently renting it can be particularly difficult to find money to set aside. You may have to decide whether returning to live with parents is an option, to save over the short term, or move into cheaper accommodation.

History shows that house prices can dip, particularly during difficult economic periods. Every six months set aside some time to see how the market is performing in the area you want to buy. You may find that property prices are stagnating, or even falling, and you have greater bargaining power as a first-time buyer without a property to sell.

If you are willing, expand your search. House prices could fall in some areas, but not others, and perhaps your needs and preferences will change over the time you are saving for a deposit. This could mean the goal of home ownership is within reach sooner than expected.

First time buyer tips

Saving tools