Falling foul of regulators can be expensive as a string of banks have learnt to their cost. Research from policy resource centre Good Jobs First in June found that banks and other financial services firms globally had forked out more than $160 billion in fines since 2010. And that was before Deutsche Bank was told to pay $14 billion for misselling mortgage securities in the United States.

Companies are far less likely than banks to be hit with a fine the length of a telephone number. Nevertheless, treasurers still need to navigate the world of financial regulation carefully if they are to spare their employer bad press, strategic risks and unexpected penalties.

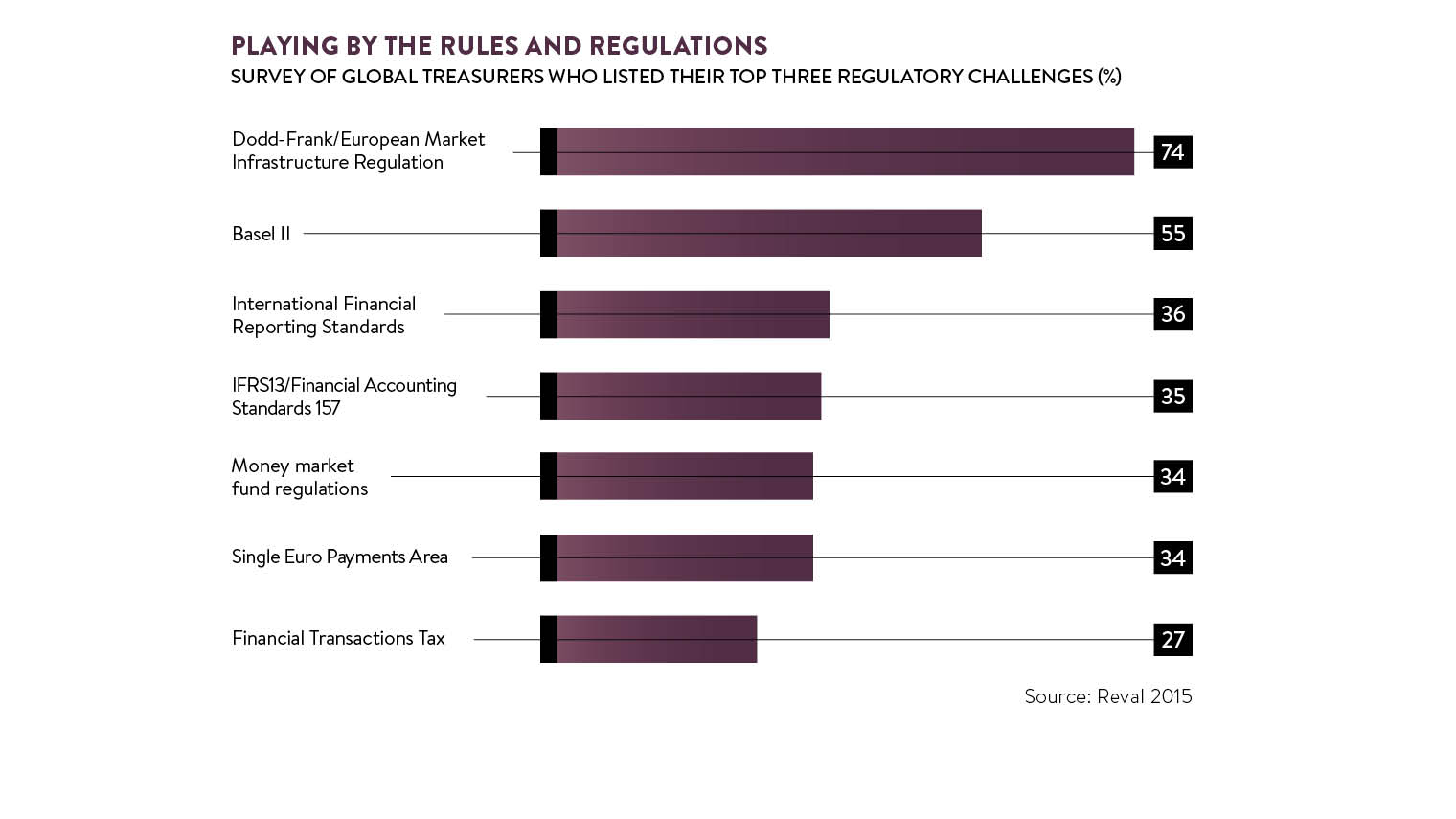

“Regulation is omnipresent,” says Richard Abigail, group treasurer of engineering consultancy Arup. “Much of the regulatory pressure on us comes through the banking sector. Regulations on the banks transfer on to corporates. We have to do more and more to be regulatory compliant.”

Mr Abigail cites the know-your-customer rules, which are designed to prevent money laundering, as onerous for treasury. Banks want far more detail on the company than in the past, including turnover, the countries the company transacts with at both group and subsidiary level, and heightened information about individual signatories.

Capital and liquidity ratios imposed on banks by Capital Requirements Directive IV (CRD IV) also have implications for treasury since banks are retreating from riskier markets and products, and are reluctant to hold short-term cash.

“Treasurers need to understand the impact of banking regulations on the banking model,” explains Yann Umbricht, head of the treasury group at professional services giant PwC. “Because of CRD IV and other regulations, banks don’t want to accept deposits and do cash-pooling arrangements in the same way as in the past. It’s getting harder to access liquidity on a centralised basis and in an easy manner.”

Breaking banking sanctions

Sanctions on countries such as Cuba, Iran, North Korea and Sudan pose another headache for treasurers. Banks are very wary of processing any transaction that could conceivably put them in breach of sanctions. This is unsurprising given the US Justice Department handed down an $8.9-billion fine to French bank BNP Paribas for sanction breaches in 2014. “Trying to get a bank to process a transaction in Iran is almost impossible,” says Mr Abigail.

If a corporate breached sanctions, it could be fined by the US Office of Foreign Assets Control or the UK Office of Financial Sanctions Implementation. Furthermore, it would probably lose its banking relationships since banks wouldn’t want to work with a company known for breaching sanctions and valuable customer relationships would be compromised.

Treasurers need to understand the impact of banking regulations on the banking model

“Our clients don’t want their consultant exposed in the press as a sanctions breaker,” says Mr Abigail. “So we update our policies, do education programmes and make sure that everyone internally is aware of what the sanction guidelines are. We bid for projects all over the world so it’s horribly complex.”

Tax avoidance

Tax is an obvious area of concern for treasurers in light of the continuing controversies surrounding multinationals such as Apple and Google. It has also been the focus of concerted international collaboration as a result of the Organisation for Economic Co-operation and Development’s Base Erosion and Profit-Shifting initiative, more popularly known as BEPS. This aims to tackle tax avoidance strategies where companies artificially shift profits to low-tax or no-tax locations.

“BEPS has heightened transparency around how our inter-company loan process works,” says Mr Abigail. “So our tax team is having to look at treasury transactions in a greater level of detail. We have to make sure we’ve got the right documents in place to support our transactions on an inter-company basis.”

Where companies lack appropriate documentation, they could find that local authorities challenge their tax returns, potentially resulting in large tax bills and penalties.

“Tax has the greatest potential for financial penalties to be levied on businesses,” says Bob Stark, vice president of strategy at treasury and risk software provider Kyriba. “Regulations are always changing and companies are always trying to find ways to minimise the amount of tax they pay to preserve the value of their organisation for investors. If you offer an interpretation that’s not accepted by the tax agencies, you risk having to pay extra tax and a fine.”

Volatile markets

Looking ahead, there is no sign that the risk landscape is about to become any easier for treasurers to navigate. Sterling has been extremely volatile since the UK voted to leave the European Union and Mr Umbricht believes this emphasises the importance of treasurers being transparent around their currency hedging programmes.

“Some people buy shares because they want to be exposed to a particular currency,” he says. “If a company hasn’t told the market that it is hedging a risk, then it announces in its results that it hasn’t benefitted from a currency movement due to hedging, it could suffer damage to its reputation.”

Mr Abigail worries that Brexit could make it much harder for treasurers to do their day jobs. “Today we can move money across Europe without even thinking about it,” he says. “Will the UK coming out of Europe result in regulation that complicates what is currently a simple transactional process?”

Protectionism is another area of concern, according to Mr Stark. “Combine protectionism with the notion that regulation solves all problems and you create a scenario where it is very difficult for everyone from the chief executive downwards to operate and plan appropriately,” he says.

Given how much uncertainty exists, how can treasurers manage regulatory risk effectively? “Collaboration is your biggest friend,” advises Mr Stark. “Treasury practices should not make it difficult for tax and accounting to fulfil their roles. On the flip side, tax and accounting should not hinder treasury’s ability to make best use of the organisation’s assets.”

Mr Abigail emphasises that treasurers need to understand regulation and what their organisation needs to do to comply with it. For example, Arup built a reporting tool into its treasury management system so it could comply with the requirement to report derivative transactions under the European Market Infrastructure Regulation. “You need to understand your organisation and how you manage the risk,” he says. “Then policies and procedures follow on the back of that.”

Ultimately, Mr Umbricht doesn’t believe that treasurers have to fall victim to upcoming regulation. Instead they can positively influence it. “Some organisations invest a lot of time in trying to influence the implications of proposed regulations,” he says. “Only at that point in time can you have a say and change the potential outcome.”

Breaking banking sanctions